CARLSBAD — The city’s draft budget once again is in the black, even with a request for 39 new positions.

Many of those positions are additions to departments which have not seen an uptick in personnel in 10 or 20 years. City Manager Scott Chadwick said the increased headcount will not be a trend, but it turned heads nonetheless.

The new employees will come in under a reformed pension schedule, which expects to see long-term benefits. Under the old system and thanks to the Great Recession, many cities in the state are struggling to meet their pension debt liabilities.

“We have to be planning out into the future to pay down this unfunded liability you don’t see in the budget,” Carlsbad Assistant City Manager Laura Rocha said. “That’s actually in our balance sheet.”

Carlsbad instituted its own reform in 2010, knocking down its per employee contribution. The state, meanwhile, has undergone a couple of reforms, but lowered the rate to in 2013.

What it means for Carlsbad is it will help the city reach its goal of 80% funded over the next several years, according to Chadwick and Rocha.

The formula is the percentage of an employee’s salary multiplied by the number of years served and the age when an employee receives the full amount, the two said.

“There are many factors that go into what ultimately becomes our payment,” Chadwick said.

Carlsbad has three tiers — one for employees who’ve been in the system prior to the reforms, which is a rate of 3% and retirement age of 60. The second tier is 2% at 60, while the third tier (by the state) is 2% at 62 as a result of the Public Employees’ Pension Reform Act (PEPRA), which took effect in 2013.

The city pays per employee on pensionable wages. Overtime wages are not applied to the pension payments.

Kristina Ray, the city’s communications director, said another key change was the pension is now calculated based on the average salary over the past three years rather than the single highest year’s salary

“This helps prevent “spiking,” or an employee taking a much higher paying job for the last 12 months of employment to get a higher pension benefit,” she said.

The city has two funds — a miscellaneous and safety. Per Chadwick’s budget presentation several weeks ago, the miscellaneous plan is 74% funded and safety is 72% funded.

Also, the city has made several substantial payments over the past several years including $10 million in a pension stability fund, $9 million in Fiscal Year 2016-17 and $11 million last year.

In addition, Rocha and Chadwick proposed a $20 million payment for the 2019-20 fiscal year to save $11 million in interest over the next 17 years, along with saving $2.5 million in payroll obligations, Rocha said.

Chadwick and Rocha are also proposing a City Council policy ensuring debit obligations.

State view

For years, local leaders have howled at the state’s discount rate, which is the expected return on the pension investments. If the returns come in lower than the set rate, then local entities are on the hook for a larger contribution.

In addition, Rocha said the state’s projections of its rate return is about 18 months behind, meaning local municipalities within CalPERS have an even more difficult challenge with their budget projections and obligations.

“To develop the 2019-20 budget, we have to do some of our own assumptions … based on activity CalPERS has put out and whether they met their market rates,” Rocha said.

The state releases an actuarial report, the last coming in June 2017, which ties the city to its obligations, along with the city adjusting its budget as needed.

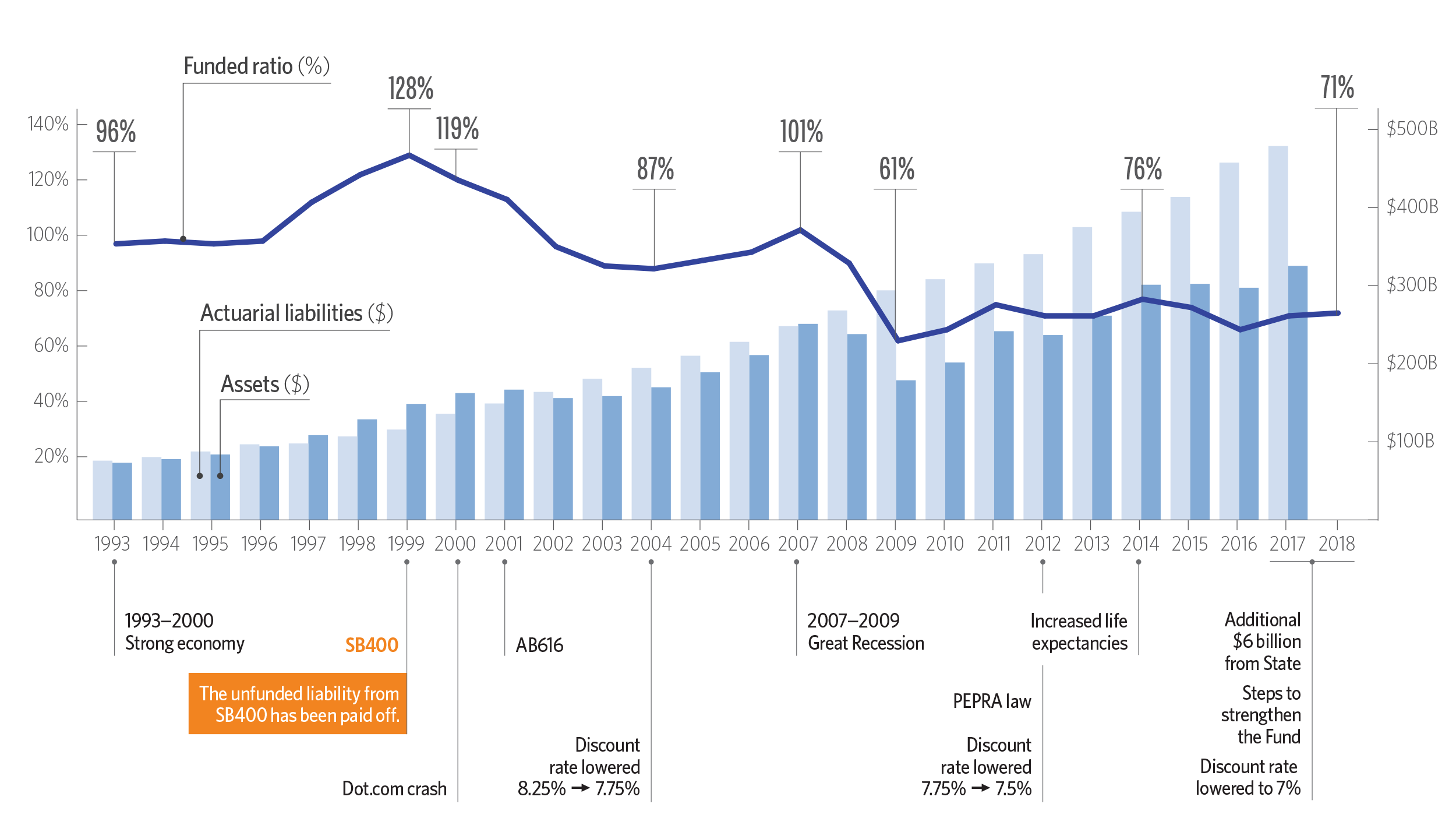

In 2013, CalPERS lowered the discount rate from 7.75% to 7.5%, along with a shorter amortization (gradual reduction of debt) from 30 years to 20 years. However, the state again lowered the discount rate in 2017 to 7% due to pushback from municipalities across the state.

CalPERS has been up and down the past 20 years. Its funded ratio was 128% in 1999, but then the dot-com crash hit, lowering the fund to 119% in 2000. By 2004, CalPERS was at 84% before rising to 101% in 2007.

Then the Great Recession hit and the fund plummeted to 61% and has been trying to recover ever since.

“When they do not earn 7%, like they did several years ago, pension plans were suffering,” Rocha said. “The interest returns weren’t there in the plans to make up for that. That’s where employers have had to step up and pay these higher contribution rates.”

As for the assets and actuarial liabilities, the funds assets were about 10% more than the liabilities in 1999. Three years later, though, the liabilities had overtaken the assets and the gap between the two has grown.

Actuarial liabilities occur when a fund’s present value exceeds the future payouts.

By 2009, the Great Recession had taken its toll as CalPERS had about $100 billion more in liabilities than assets. And now, it’s even more at about $150 billion.

CalPERS has more than 1.9 million public sector workers in the retirement program, and provides healthcare for 1.4 million. Of those 1.9 million members, 38% are school members and 31% each in public agencies and the state.

It has an investment portfolio of $354 billion, as of 2018, with a $1.6 billion budget to administer the system. CalPERS projections were at an 8.6% percent net return on its investments in the 2018-19 fiscal year.

Over the 2016-17 and 2017-18 fiscal years, the Public Employees’ Retirement Fund (PERF) saw a 3% increase from 68% to 71%. It also included a $6 billion contribution by the state.

Every dollar paid to retirees comes from three sources: investment earnings ($0.59), CalPERS employers ($0.28) and CalPERS members ($0.13). The fund pays out $21 billion in benefits annually.

{kind=link}